Personal Injury Protection (PIP) insurance in Florida can be confusing, especially with the state’s “no-fault” system and strict 14-day rule. Florida’s no-fault law simply means realizing who opens their wallet first, not who caused the crash. Instead of waiting months for the guilty driver’s company to accept blame, your own policy acts as a financial first responder to quickly pay your initial medical bills.

Picture two drivers involved in identical fender benders during their morning commute. Sarah visits a doctor on day three for a stiff neck, safely activating her Personal Injury Protection coverage. Mike decides to tough it out, hoping his back pain fades, and finally visits a clinic on day fifteen. Because Mike missed the critical 2 week window, his carrier pays absolutely nothing for his recovery.

Industry data reveals that delaying treatment is a primary reason drivers lose their mandatory benefits. You must seek medical care immediately, as violating the strict Florida 14-day rule for car accidents legally allows your insurer to deny coverage entirely. Securing this vital funding requires understanding this ticking clock, ensuring your financial safety net doesn’t vanish when you need it most.

Meet Your Insurance “First Responder”: How PIP Covers You Regardless of Fault

You’ve heard Florida is a “No-Fault” state, but that doesn’t mean crashes happen without anyone to blame. It just means your own Florida auto insurance policy pays your medical bills first, regardless of fault. To legally register a vehicle here, you must meet the mandatory minimum auto insurance requirements by carrying $10,000 in Personal Injury Protection (PIP). Think of Personal Injury Protection (PIP) as an emergency medical fund built right into your monthly premium.

Because PIP acts as your “Primary Payer,” it jumps ahead of your regular health insurance. If you get rear-ended on your daily commute, the hospital won’t bill your private medical provider right away. They bill your personal injury coverage first. This rule ensures you get treated quickly without waiting months for insurance adjusters to argue over who caused the wreck.

While this $10,000 safety net is required by law, accessing those funds requires playing by a strict set of rules. Your coverage isn’t automatically guaranteed just because you were in an accident, which brings us to the strict timelines that govern your payouts.

The 336-Hour Ticking Clock: Why Waiting to See a Doctor Could Cost You $10,000

Adrenaline often masks pain immediately after a crash, leading to the common mistake of “waiting to see if it heals.” However, under the Florida 14-day rule for car accidents, delaying treatment is a massive financial hazard. You have exactly two weeks from the date of the collision to receive “Initial Services and Care,” or your car accident insurance company can legally deny your medical benefits entirely.

Securing this baseline coverage doesn’t mean you need immediate surgery. Figuring out how to file a PIP claim in Florida starts simply by getting an official medical evaluation to document your crash-related injuries. The state strictly dictates who is allowed to perform this initial exam to keep your coverage valid.

Walking into a massage therapist or an acupuncturist’s office won’t satisfy this strict legal requirement. To protect your coverage, your first visit must be with one of these qualified medical providers:

- Emergency Room doctors or urgent care physicians

- Medical Doctors (MDs) or Doctors of Osteopathy (DOs)

- Licensed Chiropractors

- Dentists (for accident-related dental trauma)

Beating that two-week deadline successfully opens the door to your Personal Injury Protection (PIP) benefits, guaranteeing you at least $2,500 in coverage. But unlocking your full policy limit requires a more serious diagnosis.

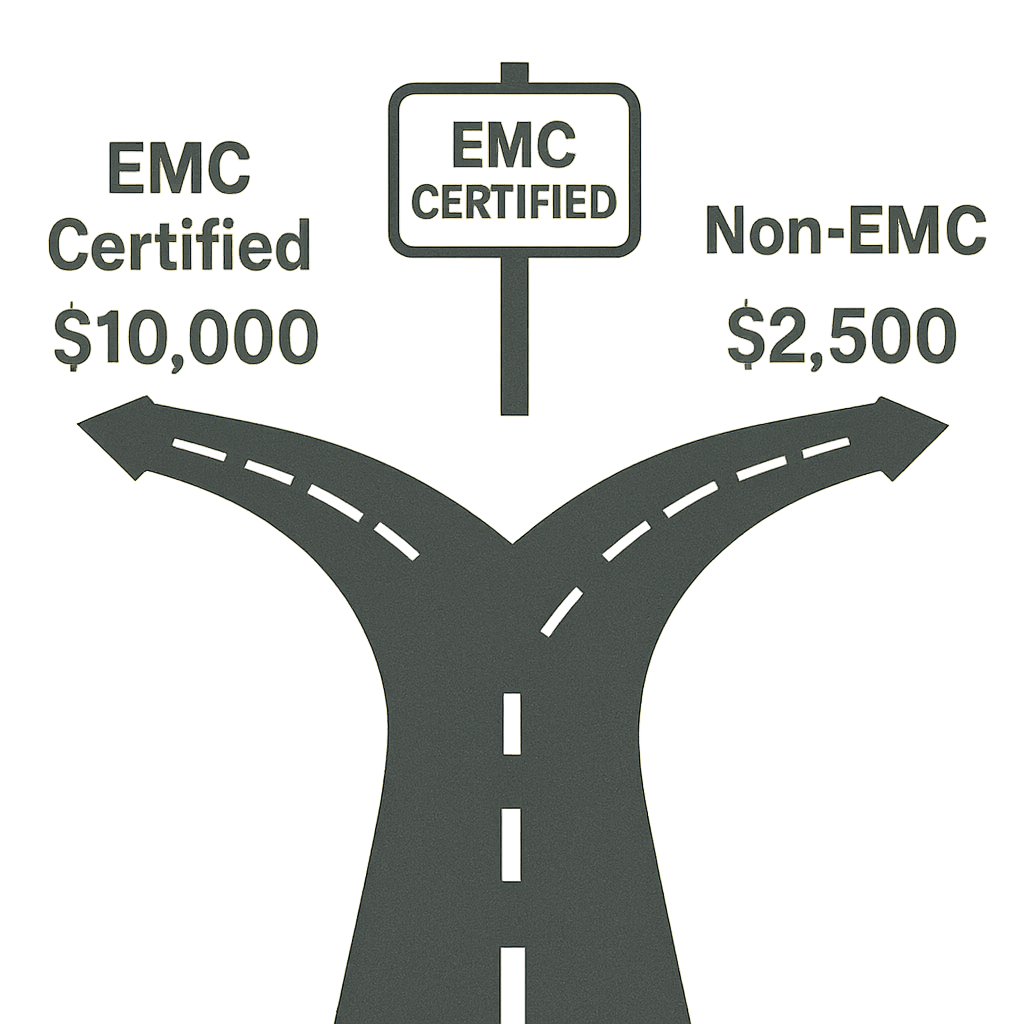

From $2,500 to $10,000: How the “Emergency Medical Condition” Gateway Controls Your Payout

Beating the 14-day clock activates your coverage, but it doesn’t mean your bills are paid at 100%. Think of Personal Injury Protection (PIP) as a heavy-duty discount code. Under the Florida 80 percent medical coverage rule, your auto insurance pays exactly 80% of your eligible medical bills, leaving you or your health insurance to handle the remaining 20%. If an initial hospital bill is $1,000, your PIP pays $800.

Unlocking your maximum $10,000 limit requires a specific medical “key.” According to Florida statutes section 627.736, a qualified doctor must officially declare your injury an Emergency Medical Condition. The emergency medical condition definition Florida recognizes requires proof that your overall health would be in serious jeopardy without immediate care, such as severe, lingering whiplash or a fractured bone.

Failing to get that critical EMC stamp of approval means your insurance company legally caps your medical reimbursement at just $2,500—even if your actual recovery bills are much higher. Securing the proper diagnosis ensures you aren’t stuck paying out-of-pocket for expensive medical care.

More Than Just Medical Bills: Using PIP to Recover Lost Wages and Funeral Costs

Missing work adds financial stress, but your policy acts as a partial paycheck replacement. Does Personal Injury Protection (PIP) cover lost wages? Yes, your Florida car insurance reimburses 60% of your gross income. If you typically earn $1,000 weekly, PIP pays out $600 to help keep the lights on, drawing directly from your available $10,000 limit.

Securing these funds requires more than just calling your boss; you must provide formal proof. The insurance company needs two specific items to process your claim:

- A Wage and Salary Verification form completed by your employer detailing your recent earnings.

- A doctor’s disability note explicitly stating that your injuries prevent you from doing your job.

Tragically, fatal crashes happen, making recovering funeral expenses through Personal Injury Protection (PIP) a necessary lifeline for grieving families. Florida policies include a separate $5,000 death benefit per person—paid on top of medical limits—to help handle burial costs.

Protecting Your Family and Pedestrians: Who Exactly Does Your PIP Policy Shield?

Most drivers assume their policy only activates behind the wheel. However, your florida auto insurance acts like a financial umbrella over your entire household. If your spouse or children living with you are injured in a crash—even while riding in a friend’s vehicle—your policy steps in as their first responder to pay those medical bills.

This safety net extends far beyond the car’s interior. If you are struck by a vehicle while walking the dog or riding a bike, PIP coverage for pedestrians and cyclists immediately kicks in. Even outside a motor vehicle, your personal policy treats the incident exactly like a typical crash, securing your right to medical care and lost wages.

Riding in someone else’s car adds a slight twist to Personal Injury Protecting Auto Insurance coverage in Florida. If you are an injured passenger without your own policy, the host driver’s insurance will cover you. But what happens if your medical bills climb way past these built-in limits? It becomes vital to know your next steps when that initial $10,000 simply isn’t enough to fully heal.

When $10,000 Isn’t Enough: Navigating Deductibles and Suing for Pain and Suffering

Before your policy pays out, you must clear your deductible—think of it like a cover charge. When weighing your personal injury protection deductible options, remember that a $1,000 deductible is subtracted directly from your $10,000 limit, leaving exactly $9,000 to fund your 80% medical reimbursements.

Once those limited benefits run dry, you must look to the at-fault driver’s insurance to cover the remaining gap. This highlights the core difference of PIP vs bodily injury liability: your PIP handles your immediate bills regardless of who caused the crash, while the at-fault driver’s Bodily Injury Liability covers the ongoing harm they inflicted on you.

Stepping outside the no-fault system to demand more money requires meeting Florida’s strict “Serious Injury Threshold” (also known as a tort threshold). To legally succeed in suing for pain and suffering in Florida, your injuries must include at least one of the following:

- Significant and permanent loss of an important bodily function

- Permanent injury within a reasonable degree of medical probability

- Significant and permanent scarring or disfigurement

- Death

Knowing these legal boundaries prepares you for the road ahead, and your immediate post-crash decisions dictate your success.

Your 3-Step PIP Action Plan: Securing Your Recovery After a Florida Crash

To achieve financial peace of mind and unlock your Florida no-fault insurance benefits, follow this immediate action plan on how to file a Personal Injury Protection (PIP) claim in Florida:

- Seek medical care within 14 days: See a doctor quickly so your insurer cannot legally deny your coverage.

- Notify your insurer: Report the accident promptly to activate your Florida car insurance.

- Document everything: Organize all medical bills and visit summaries to prevent frustrating claim denials.

Once comfortable taking these initial steps, you will view PIP not as a confusing legal hurdle, but as a protective tool you actively control. If your medical needs eventually grow and your $10,000 in benefits are exhausted, remember you don’t have to face the remaining bills alone—reaching out for professional legal help is a confident next step.

Do You Have Questions Regarding Your Insurance Needs?

Call us and let our knowledgeable team of award-winning insurance agents help. We provide a wide range of affordable insurance solutions for people from all walks of life. Whether you are seeking insurance for your home, auto, business, life, or health, our team of licensed insurance agents will help you find the best coverage for your specific needs at the best possible rates.