How Uninsured Motorist Insurance Protects You

You are a safe driver who pays your premiums on time, but what happens when the person beside you does not? According to the Insurance Research Council, roughly one in eight drivers on the road has no coverage at all. Getting hit by one of them quickly turns a simple commute into a massive financial crisis.

Many people mistakenly believe “full coverage” protects them against every possible scenario. In reality, your basic liability coverage acts strictly as a shield for other people if you cause a crash. It does nothing to pay your own medical bills if an uninsured driver causes the accident.

That is exactly where Uninsured Motorist Insurance steps in to save your bank account. Think of this protection as a personalized safety net you lay down for yourself. Instead of draining your savings for a $15,000 emergency room visit after a hit-and-run, this backup policy covers the costs the at-fault driver cannot.

Recognizing this coverage gap safeguards your finances. As you explore your auto insurance options, a proactive look at your current declarations page will reveal whether you actually have your own back.

The Safety Net: What is Uninsured Motorist Coverage?

You already know your standard liability insurance pays the other person’s bills if you cause a wreck. Think of Uninsured Motorist Insurance coverage as a shield protecting other drivers from your mistakes. But what happens if someone plows into your car without a dime of insurance? Suddenly, that liability shield does absolutely nothing to fix your broken arm or damaged bumper.

This exact scenario is why uninsured motorist insurance exists. While liability is a “third-party” benefit meant for someone else, this coverage is a “first-party” financial safeguard designed strictly to protect you. Instead of waiting on a hopeless lawsuit against a broke driver, you can tap into immediate funds for your emergency room visit.

By relying on this provision, your own insurance company acts as a stand-in for the irresponsible driver. They step into the shoes of the person who hit you, paying exactly what the other driver legally owed. Figuring out what to do if an at-fault driver lacks coverage is incredibly simple when your own policy automatically absorbs that $15,000 medical bill.

Guarding against entirely uninsured drivers is crucial, but they aren’t the only financial hazard on your daily commute. Often, the person who hits you has an active policy, but it simply isn’t large enough to cover your recovery. Handling that specific shortfall requires bridging the gap: the difference between Uninsured Motorist (UM) and Underinsured Motorist (UIM) protection.

Bridging the Gap: The Difference Between UM and UIM Protection

Many drivers assume they are perfectly safe if the person who hit them carries an active policy. But what if that driver only bought the bare state minimum allowed by law? Uninsured Motorist (UM) protects you when the at-fault driver has zero coverage, while Underinsured Motorist (UIM) steps in when they have insurance, just not enough to pay your medical bills. This underinsured protection bridges the gap between what they can pay and what you actually need.

Distinguishing between Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage protects your wallet against major injuries. Here is exactly how a UIM “shortfall” claim handles partial coverage:

- The Bill: You face a $50,000 hospital bill after a bad intersection crash.

- The Limit: The at-fault driver’s policy maxes out at a $25,000 payout.

- The Shortfall: Your UIM coverage kicks in to pay the remaining $25,000 difference.

Securing this supplemental gap coverage ensures your physical recovery isn’t limited by a stranger’s cheap policy choices. At least with an underinsured driver, someone actually stayed at the scene to hand over their insurance card. But what happens to your coverage when the person who caused the wreck speeds off before you can even catch their license plate?

When They Disappear: How to Handle a Hit and Run Claim

Watching a car speed away after sideswiping you is a terrifying experience. Insurance companies officially designate these fleeing motorists as “untraceable drivers.” Fortunately, your uninsured motorist insurance (UM) policy treats them exactly like someone with zero coverage, creating a reliable backup plan for recovering medical expenses from an untraceable driver. This policy also steps up to provide vital protection for passengers in a hit and run accident.

Because your insurer needs proof another vehicle actually caused the crash, knowing how to file a hit and run claim means acting fast. Follow this immediate checklist at the scene:

- Call 911 to secure an official police report.

- Take clear photos of the damage, highlighting any foreign paint transfer.

- Gather contact information from bystanders who witnessed the event.

Once this essential evidence is secured, paying your hospital bills becomes much easier. Yet, physical injuries are only half the battle after a sudden collision; you also have to manage the costly property damage to your vehicle.

Bodily Injury vs. Property Damage: Protecting Your Health and Your Car

Surviving a crash brings immense relief, but the aftermath splits into two expensive problems: physical injuries and a smashed vehicle. Uninsured motorist insurance tackles this by dividing your protection into two distinct categories.

Uninsured Motorist Bodily Injury (UM-BI) steps in to pay for hospital stays and lost wages. Separating your bodily injury and property damage limits is vital because medical debt escalates much faster than mechanic bills. This serves as your essential financial buffer.

Fixing the car itself falls under Uninsured Motorist Property Damage (UM-PD), though many drivers rely on their standard collision policies instead. If you do, secure a collision coverage deductible waiver. This simple add-on ensures you avoid paying a $500 out-of-pocket penalty for someone else’s careless mistake.

Trusting basic state mandatory liability requirements often leaves you dangerously exposed to massive shortfalls. Because minimum laws only dictate what the at-fault driver must carry, your personal protection depends entirely on your own choices. Seeing these minimums fail in real time reveals the true stakes, particularly in high-risk regions.

Why Florida Drivers Face Higher Risks: A Local Case Study

Living here means sharing the road with a staggering number of illegally uninsured drivers. You might think your state-mandated Personal Injury Protection (PIP) fully shields you. However, PIP hides a dangerous trap: it caps your medical payout at just $10,000. You can easily blow past that limit during a single trip to the emergency room.

When that basic limit runs dry, the true difference between PIP and underinsured protection becomes painfully clear. PIP acts as a small, immediate starter fund, but your underinsured coverage is the heavy-duty backup. If a careless driver leaves you needing a $40,000 surgery, this supplemental layer swoops in to cover the massive $30,000 shortfall they caused.

Adding Florida uninsured motorist insurance costs a bit more, but it remains the smartest financial move to protect your savings. It guarantees someone else’s reckless mistake won’t bankrupt your family. Once you realize how essential this backup layer is, the next logical step is figuring out how to maximize it across multiple vehicles.

To Stack or Not to Stack: Multiplying Your Protection

If you own more than one vehicle, your policy holds a hidden superpower. Stacking auto insurance policies simply means layering your protection. Instead of each car having its own isolated coverage, you combine them to build a taller, stronger wall against devastating medical bills.

Many drivers ask if this upgrade makes financial sense and is supplemental coverage worth the cost? Let’s look at a two-car family with a $50,000 uninsured limit per vehicle:

- Unstacked (Standard): Costs slightly less each month, but caps your maximum payout at just $50,000 if an uninsured driver hits you.

- Stacked (Layered): Costs a few extra dollars, but stacks the limits of both cars together, giving you $100,000 in total protection.

Maximizing your coverage limits without buying an entirely new policy is usually the smartest financial move for a multi-car household. Once you secure this reinforced protection, the final hurdle is actually using it without worrying about your rates jumping.

Filing a Claim Without Fear: Premiums and the Subrogation Process

Many drivers hesitate to use their coverage because they fear their monthly bill will skyrocket. Fortunately, a premium increase after filing a non-fault claim is incredibly rare. Because you are the victim of someone else’s mistake, your provider steps in as a financial shield rather than penalizing you for an accident you couldn’t prevent.

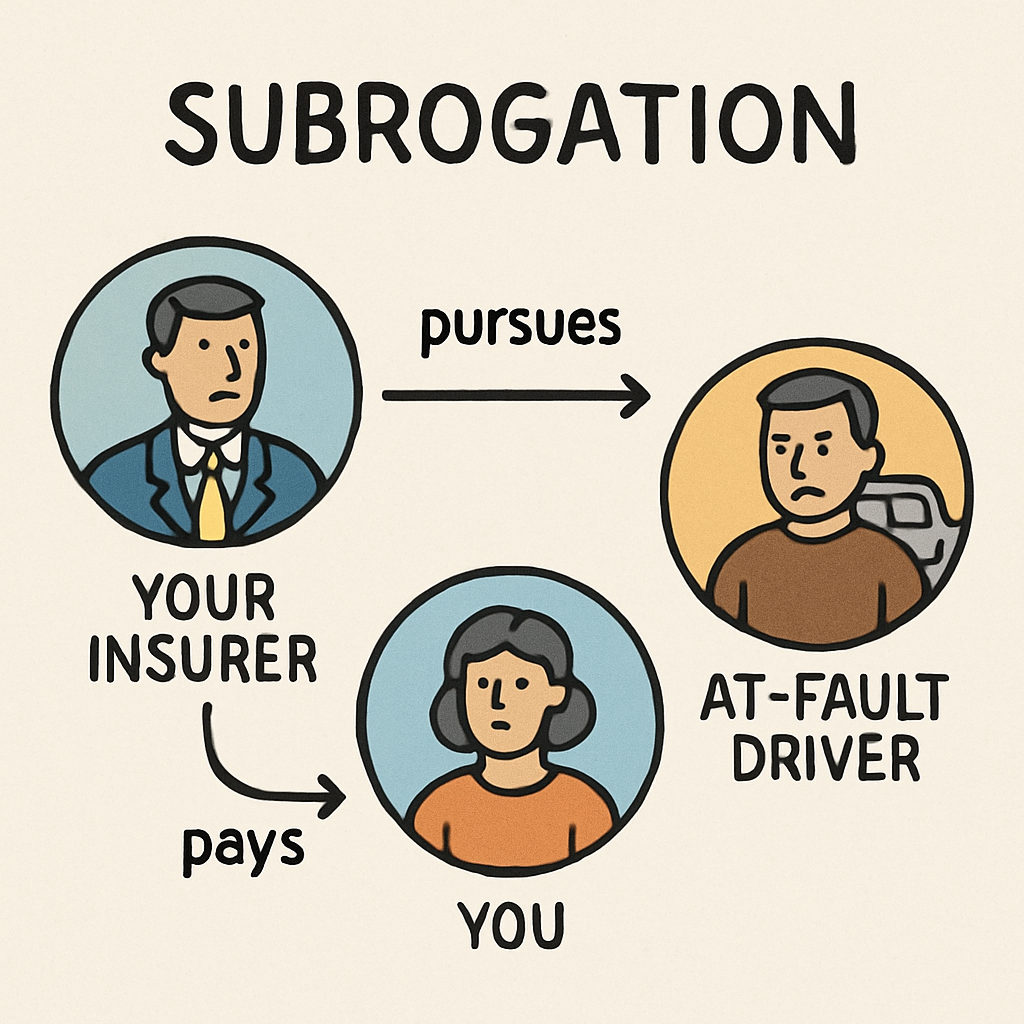

Behind the scenes, your insurer isn’t just accepting the financial hit. They automatically initiate the subrogation process in car insurance claims—a legal term meaning they pay you immediately, then hunt down the at-fault driver for reimbursement. If the uninsured driver has hidden assets or eventually gets a job, your company handles the chase, ensuring you aren’t waiting years to fix your car or pay the hospital.

Occasionally, insurance companies disagree on exactly who owes what. Instead of dragging you into an expensive lawsuit, they resolve this using arbitration for insurance settlement disputes. A neutral third party reviews the accident details and decides the final payout behind closed doors, keeping you completely out of the courtroom.

Your 3-Minute Policy Check-Up

You no longer have to cross your fingers and hope the driver next to you carries enough coverage. By taking control of your auto insurance options, you are building a personal safety net instead of relying on a stranger’s. Does your current policy actually have your back, or just the back of the person you hit?

To find out, take three minutes right now to perform a quick DIY audit:

- Locate your policy’s Declarations Page online or in your paperwork.

- Find the ‘Uninsured Motorist’ line item.

- Compare that limit to your health insurance deductible to ensure your potential out-of-pocket costs are covered.

Increasing this coverage is often the cheapest part of your premium, yet it offers the most vital protection. If disaster strikes, this reliable coverage is infinitely faster and more secure than pursuing messy legal options against drivers without insurance, giving you true financial peace of mind.

Do You Have Questions Regarding Your Insurance Needs?

Call us and let our knowledgeable team of award-winning insurance agents help. We provide a wide range of affordable insurance solutions for people from all walks of life. Whether you are seeking insurance for your home, auto, business, life, or health, our team of licensed insurance agents will help you find the best coverage for your specific needs at the best possible rates.